Sterling Infrastructure’s Growth Story: Strong Fundamentals, Tight Valuation

Sterling Infrastructure’s rapid growth is driven by data centers and reshoring, but its valuation may already reflect much of that upside.

Sterling Infrastructure (NASDAQ: STRL) has quietly transformed from a traditional civil construction contractor into one of the most compelling growth stories in U.S. infrastructure. The bullish case today rests on a powerful combination of accelerating earnings, expanding margins, and structural demand tailwinds - particularly from data centers, semiconductors, and reshoring.

At the core of the investment thesis is growth. Sterling delivered $2.49 billion in 2025 revenue, representing roughly 18% reported growth (32% adjusted), alongside a 53% surge in adjusted EPS to $10.88. This is not just top-line expansion - it’s highly profitable growth. Adjusted EBITDA margins exceeded 20% for the first time, reflecting a deliberate shift toward higher-value, less commoditized work. Over a longer horizon, the company has compounded EPS at an impressive ~44% CAGR since 2019, underscoring consistent execution.

The most important driver behind this transformation is Sterling’s E-Infrastructure segment. This division—focused on mission-critical projects like data centers and semiconductor facilities—has become the company’s economic engine. In 2025 alone, the segment grew 59% and now accounts for nearly 60% of total revenue. Even more striking, mission-critical work makes up roughly 84% of backlog within the segment, signaling sustained demand visibility.

This shift is critical because E-Infrastructure carries structurally higher margins than legacy construction. Sterling is no longer competing on low-bid highway contracts; it is embedded in complex, high-spec projects tied to secular megatrends like AI infrastructure and U.S. manufacturing reshoring. These trends are still early-cycle. Data center construction spending alone has surged dramatically in recent years, creating a long runway for companies positioned like Sterling.

Backlog further strengthens the bull case. Sterling exited 2025 with a record $3.0 billion backlog, up 78% year-over-year, and a broader opportunity pipeline approaching $4.5 billion. This provides unusually strong forward revenue visibility for a construction firm and supports management’s 2026 guidance of ~25% revenue growth and ~26% EPS growth. Few industrial companies offer this level of contracted growth combined with double-digit margin expansion.

Profitability trends also reinforce the story. Gross margins have steadily climbed into the mid-20% range, while operating leverage continues to drive outsized earnings growth relative to revenue. Even with slight recent margin compression on a trailing basis (~11.7% net margin), this appears more like normalization after rapid expansion than structural deterioration.

Critically, Sterling generates strong cash flow—$440 million in operating cash flow in 2025—and maintains a solid balance sheet, giving it flexibility for acquisitions and continued expansion. This financial strength reduces execution risk and supports ongoing reinvestment into higher-return segments.

From a market perspective, Sterling is increasingly being recognized as a leader rather than a cyclical contractor. The stock has dramatically outperformed, with strong relative strength and top-tier earnings ratings, reflecting institutional accumulation and confidence in the company’s trajectory.

In sum, the bullish thesis on Sterling Infrastructure is straightforward: a company executing a successful business model shift into higher-margin, structurally growing end markets, backed by record backlog and strong financials. While volatility and cyclical exposure remain risks, the combination of secular tailwinds, margin expansion, and earnings momentum suggests Sterling is not just a construction company—it’s a long-duration infrastructure growth story.

Here’s a clean, assumption-driven DCF for Sterling Infrastructure based on the most recent financials and reasonable forward estimates.

Step 1: Base financials

- Free Cash Flow (TTM): ≈ $363M

- Shares outstanding: ≈ 30.7M

- Net cash: ≈ +$41M

- Current price: ≈ $456 (market cap ~$14B)

This implies:

- FCF per share ≈ $11.8

- FCF yield ≈ 2.6% → already pricing in strong growth

Step 2: Key assumptions

Given STRL’s exposure to data centers + E-infrastructure, growth is above industrial averages, but likely to normalize.

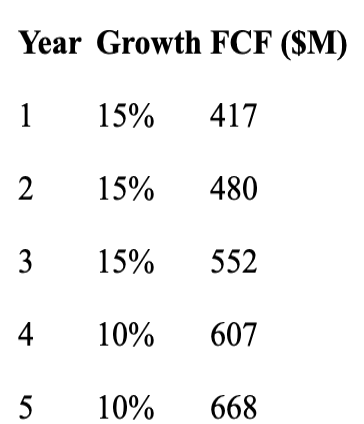

Growth assumptions (5-year)

- Year 1–3: 15% FCF growth

- Year 4–5: 10% growth

- Terminal growth: 3%

This reflects deceleration from recent hypergrowth but still strong secular tailwinds.

Discount rate (WACC)

- 9% (reasonable for mid-cap industrial with cyclicality)

Step 3: Projected FCF

Starting FCF = $363M

Step 4: Terminal value

Terminal FCF = 668 × 1.03 ≈ 688M

Terminal Value = 688 / (0.09 – 0.03)= $11.5B

Step 5: Present value

Discounting at 9%:

- PV of 5-year FCF ≈ $2.0B

- PV of terminal value ≈ $7.5B

Enterprise Value (DCF)

→ ≈ $9.5B

Add net cash:

→ Equity Value ≈ $9.55B

Step 6: Intrinsic value per share

$9.55B / 30.7M shares ≈ $311/share

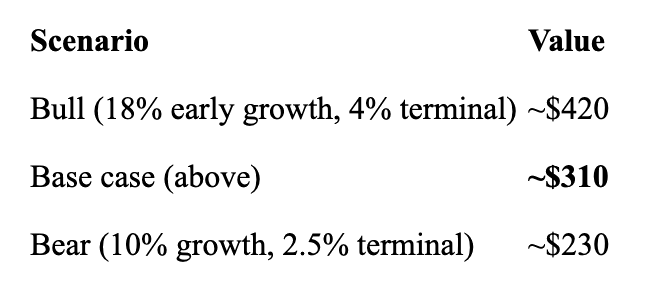

Step 7: Sensitivity (this matters a lot)

Interpretation

- Current price: ~$456

- DCF base value: ~$310

- Implied downside: ~30%

So the market is pricing in:

- Sustained high-teens growth for longer

- Continued margin expansion

- Or a structurally lower discount rate

Key insight

This is the crucial point:

Sterling is not expensive because the model is wrong—it’s expensive because:

- FCF has already scaled rapidly (from ~$100M → ~$400M in a few years)

- The market expects E-infrastructure (AI/data centers) to keep compounding at elevated rates

A standard DCF struggles with companies in mid-transition to higher-quality earnings—and STRL is exactly that.

Bottom line

- DCF says: moderately overvalued (~$310 fair value)

- Market says: this is a long-duration compounder

The gap comes down to one question:

Do you believe Sterling can sustain 15%+ FCF growth for most of the next decade?

If yes → today’s price can be justified

If no → valuation is stretched

You don’t find life-changing stocks by the time they hit the headlines.

By then, the smart money is already gone.

The biggest winners — the 10X, 20X, even 50X stocks — all share one thing in common: they were discovered early, when most investors weren’t paying attention… or didn’t understand what they were seeing.

That’s exactly where we operate.

This newsletter isn’t about chasing hype or recycling the same mega-cap names everyone already owns. It’s about identifying high-growth companies before they break out — using a disciplined framework that filters signal from noise.

Inside, you’ll get:

- Under-the-radar growth stocks with asymmetric upside

- Clear entry zones (not vague “watch lists”)

- Risk management strategies to protect your capital

- Deep dives that explain why a company could dominate its market

No fluff. No recycled headlines. No “get rich quick” nonsense.

Just high-conviction ideas built for investors who want more than average returns.

If you’re curious about whether we’re recommending Sterling to our clients, this is where you start.

👉 Join now and get immediate access to our latest high-growth pick.